Refresher on Probability and Matrix Operations

Outline

Matrix operations

Matrix operations

Vectors and summation

Vectors and summation

Probability

Probability

Definitions

Definitions

Calculating probabilities

Probability properties

Probability formulae

Random variables

Random variables

Joint Probabilities

Joint Probabilities

Definition

Independence

Conditional Probabilities

Conditional Probabilities

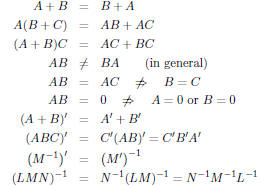

Matrix operations

Here are some of the important properties of matrix and vector

operations. You don't need to memorize them, but you should

be able to apply them to questions on your problem sets.

What's different between the matrices A, B, and C versus L,

M, and N?

Since we are taking the inverses of the latter group , they must

be square and full rank. This is known as being non-singular.

Think of the matrix as a system of equations. each row in M is

a set of coefficients for the values of a vector of unknown

variables, say r, and solutions, s. If the matrix is invertible, you

can solve Ar = s.

In the context of regression, the M matrix is our observed

covariates (usually called X), s is a vector of outcomes (y), and

r is the vector of coefficients that we are trying to find ( β).

Vectors and summation

Define l as a conformable vector of ones.

We can express a sum in terms of vector multiplication:

We can do the same for a sum of squares of x:

Preliminary definitions

The sample space

![]() is the set of all possible outcomes of our

is the set of all possible outcomes of our

"experiment."

Note that experiment has the meaning in probability theory of

being any situation in which the final outcome is unknown and

is distinct from the way that we will define an experiment in

class.

An event  is a collection of possible realizations from the

is a collection of possible realizations from the

sample space.

Events are disjoint if they do not share a common element, i.e.,

An elementary event is an event that only contains a single

realization from the sample space.

Lastly, though getting a bit ahead, two events are

statistically

independent if

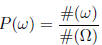

Calculating probabilities

The classical definition of probability states that, for a

sample

space containing equally- likely elementary events, then the

probability of an event is the ratio of the number of

elementary events in to that of

![]() , i.e.,

, i.e.,

The axiomatic definition of probability defines probability

by

stating that

for pairwise disjoint 1, : : : , n

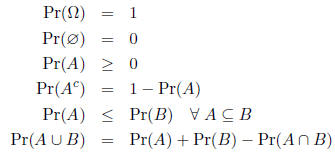

Probability properties

Let A and B be events in the sample space

![]() .

.

(Boole' s inequality )

(Boole' s inequality )

(Bonferroni's inequality)

(Bonferroni's inequality)

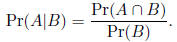

Probability formulae

The conditional probability of an event A given that an

event B

has occurred is

This equation reflects that you received additional

information

about the probability of A knowing that B occurred.

Pr(B) is in the denominator because the sample space has been

reduced from the full space

![]() to just that portion in which B

to just that portion in which B

arises.

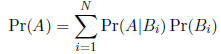

The law of total probability holds that, for a countable

partition

of  ,

,  and

and ),

then

),

then

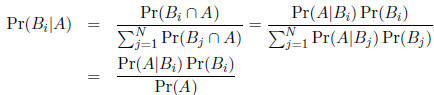

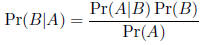

Bayes' rule states that

Bayes' rule states that

for the two event case.

Random variables

A random variable is actually a function that maps every

outcome in the sample space to the real line . Formally,

If we want to find the probability of some subset of

![]() , we can

, we can

induce a probability onto a random variable X. Let X() = x.

Then,

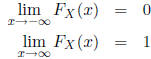

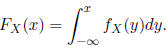

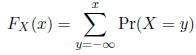

Define the cumulative distribution function (CDF),

,

as

,

as

Pr(X≤ x). The CDF has three important properties:

(i.e., the CDF is

non-decreasing)

(i.e., the CDF is

non-decreasing)

A continuous random variable has a sample space with an

uncountable number of outcomes . Here, the CDF is defined as

For a discrete random variable, which has a countable

number

of outcomes, the CDF is defined as

We can define the probability density function (PDF) for a

continuous variable as

by the Fundamental Theorem of Calculus.

It can be defined for a discrete random variable as

Note that

Joint Probabilities

Previously, we considered the distribution of a lone

random

variable. Now we will consider the joint distribution of several

random variables. For simplicity , we will restrict ourselves to

the case of two random variables, but the provided results can

easily be extended to higher dimensions.

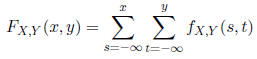

The joint cumulative distribution function (joint CDF),

![]() , of the random variables X and Y is defined by

, of the random variables X and Y is defined by

As with any CDF,  must equal 1 as x and y go to

must equal 1 as x and y go to

infinity.

The joint probability mass function (joint PMF),

is

defined

is

defined

by

The joint probability density function (joint PDF),

is

defined by

The marginal cumulative distribution function (marginal

CDF)

of  is

is

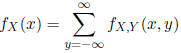

The marginal PMF of X is

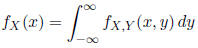

The marginal PDF of X is

You are "integrating out" y from the joint PDF.

Note that, while a marginal PDF (PMF) can be found from a

joint PDF (PMF), the converse is not true, there are an infinite

number of joint PDFs (PMFs) that could be described by a

given marginal PDF (PMF).

Independence

If X and Y are independent, then

and

Conditional Probabilities

The conditional PDF (PMF) of Y given

is defined by

As for any PDF (PMF), over the support of Y , the

conditional

PDF (PMF) must integrate (sum) to 1. It must also be

non- negative for all real values.

For discrete random variables, we see that the conditional

PMF

is

Question: What is random in the conditional

distribution of Y ,

If X and Y are independent, then

This implies that knowing X gives you no additional

ability to

predict Y , an intuitive notion underlying independence.

| Prev | Next |