Matrix Algebra Review

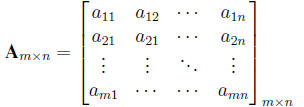

Definition. An m*n matrix, Am*n, is a rectangular array of real

numbers with m rows and n

columns. Element in the ith row and the jth column is denoted by aij .

Definition. A vector a of length n is an n*1 matrix with each element

denoted by ai. The ith

element is called the ith component of the vector and n is the

dimensionality.

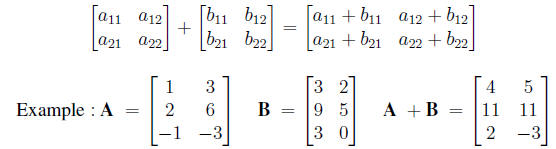

1. Two matrices A and B of the same dimensions can be added . The sum A + B

has (i, j) entry

aij + bij . So

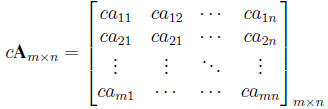

2. A matrix may also be multiplied by a constant c. The product cA is the

matrix that results

from multiplying each element of A by c. Thus

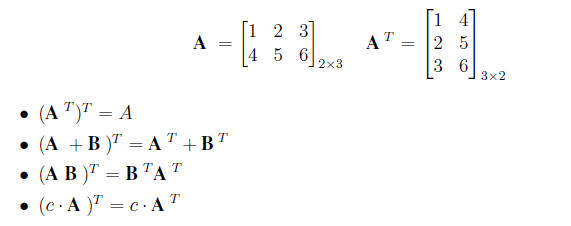

3. The transpose operation A T or A' of a matrix changes the columns into rows

so that the first

column of A becomes the first row of AT , the second column becomes second row,

and etc.

So the (i,j)th element in Am*n becomes the (j,i)th

in the transpose

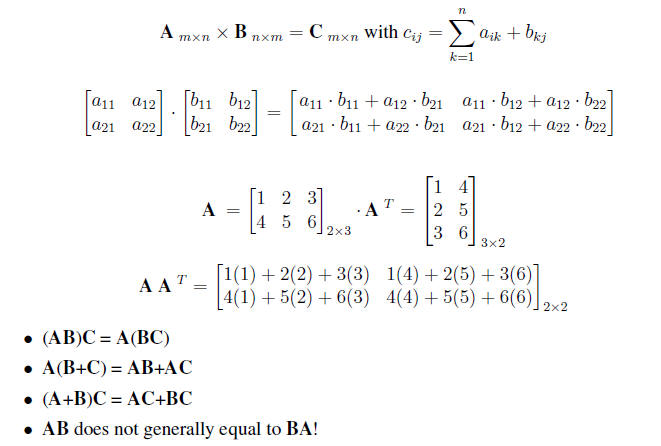

4. We can define matrix multiplication A B if the number of elements in a row

of A is the same

as the number of elements in the columns of B. E.g. when A is (p*k) and B is

(k*n). An

element of the new matrix AB is formed by taking the inner product of each row

of A with

each column of B. The matrix product AB is

Special Square Matrix

1. A square matrix A is said to be symmetric if A = AT or aij= aji for all i and j.

is symmetric,

is not symmetric

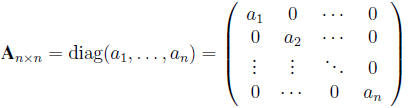

2. Diagonal Matrix.

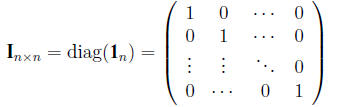

3. Identity Matrix.

The identity matrix is a square matrix with ones on the diagonal and zeros

elsewhere . It

follows from the definition of matrix multiplication that the (i, j) enrty of AI

is

.

So AI = A . Similarly, IA = A .

.

So AI = A . Similarly, IA = A .

Therefore matrix I acts like 1 in ordinary multiplication.

The fundamental scalar relation about the existence of an inverse number a-1

such that

, has the following matrix algebra extension .

, has the following matrix algebra extension .

then B is called the inverse of A and is denoted by A-1.

Other Matrix Properties

1. Trace. The sum of the diagonal elements,

2. A square matrix that does not have a matrix inverse is called a singular

matrix

The inverse of a 2*2 matrix is given by

3. A matrix is singular if and only if its determinant is 0. The determinant

of a matrix A is

denoted as |A| The determinant of a 2*2 matrix is given by

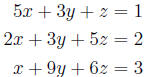

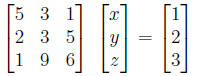

Examples 1. Simultaneous equations

We can rewrite the above three equations as a single matrix equation.

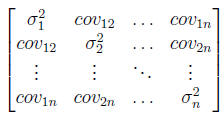

Example 2. Variance/Covariance Matrix

For a vector of random variables,

,

we can write a matrix containing their variances

,

we can write a matrix containing their variances

and their covariances. Let

be the variance of Yi and let covij be the covariance between Yi and

be the variance of Yi and let covij be the covariance between Yi and

Yj , i < j. Then the variance/covariance matrix for

is

is

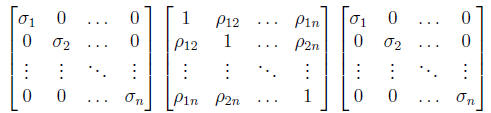

Also note that the above can be written as

where  is the

correlation of Yi and Yj . Note that all of these matrices

are symmetric. Furthermore,

is the

correlation of Yi and Yj . Note that all of these matrices

are symmetric. Furthermore,

the terms on the diagonal of the variance/covariance matrix must be positive and

terms off

the diagonal of the correlation matrix are bounded by -1 and 1.

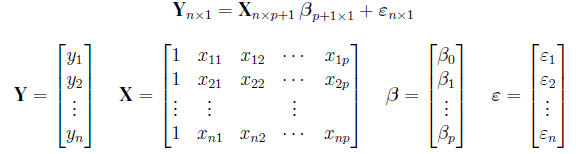

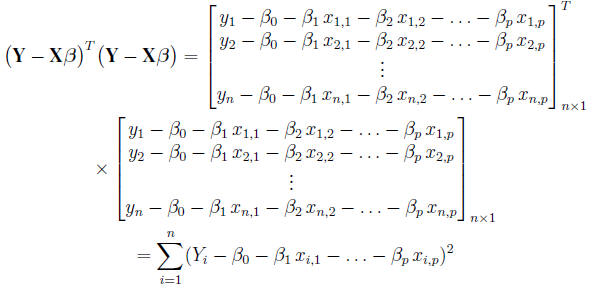

Example 3. Multiple Linear Regression

We have a response Y and a set of p independnet variables

X 1,X2, . . . ,Xp. Assume we have n

observations and for each i = 1, . . . , n observation, we assume

where  Normal (0,

Normal (0, ).

).

We can represent n observations simultaneously in matrix form as

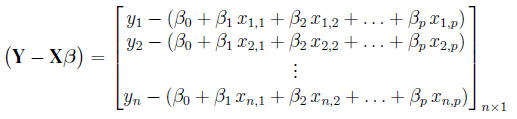

The residual  can be

written as

can be

written as

The residual sum of squares (RSS) is

Minimizing the above RSS gives the usual least -squared estimate for β

| Prev | Next |